March began with the bombings carried out by the United States and Israel on Iran, which led to sharp increases in oil and energy prices, as well as widespread declines in equity indices and, to a lesser extent, fixed income. It is not so much the conflict itself, but its impact on a key variable—energy—that has put pressure on the markets.

- S&P 500: -5,09%

- Nasdaq: -4,89%

- Stoxx Europe: -8%

- MSCI All Country World Index (EUR): -5,27% – (the dollar rose by 1.15%, so the index in USD fell by 6.11%).

- Índice global de renta fija (EUR): -0,68% – (the dollar rose by 1.15%, so the index in USD fell by 1.97%).

There is some concern among investors about a potential rebound in inflation and how it may affect upcoming interest rate decisions. Since the beginning of the conflict, the most significant movements in commodities have been:

- Oil: +62%

- Gasoline: +47%

- Diesel: +44%

- Urea: +48%

- Fertilizers: +29%

- Coal: +22%

This is not a minor move. Energy is a cross-cutting input for the entire economy, so these increases eventually filter through to overall prices.

Following multiple bombings from both sides, the current situation is one of tense calm. Trump has extended the deadline until Tuesday, April 7, for Tehran to reopen the Strait of Hormuz, while the United States, Iran, and regional mediators discuss the terms of a possible 45-day ceasefire that could lead to the end of hostilities.

Although this situation may invite optimism, this weekend President Trump has toughened his tone, threatening to destroy key Iranian infrastructure if no progress is made. For its part, Iran has rejected the ultimatum to reopen the Strait of Hormuz, stating that it will only fully resume operations once war damages are compensated. In short, calm, but very fragile and highly dependent on political decisions that are difficult to anticipate.

Consequences of higher inflation

As we mentioned in the February report, there were already signs that inflation was not fully under control and could rise again, partly due to high global deficits. The increase in gold prices can also be interpreted in this context, either as a reflection of excessive public spending or as a gradual loss of confidence in currencies. The fact is that, at the end of the month, we saw a rise in inflation expectations in the United States, something the market had not priced in for some time.

If we add to this the increase in commodity prices caused by the war, it is reasonable to think that upcoming inflation data releases may surprise to the upside. And, as is often the case, the market does not wait for confirmation—it starts adjusting in advance.

Inflation has negative consequences for both households and companies, as it reduces purchasing power. In addition, it may lead to interest rate hikes, with clear implications:

- Household: the cost of loans and variable-rate mortgages increases.

- Companies: financing becomes more expensive and margins are compressed.

- Government: deficit financing becomes more expensive, although inflation benefits highly indebted governments by reducing the real burden of debt.[1]

- Investment value: valuations decline.

This last point is especially relevant and often poorly understood.

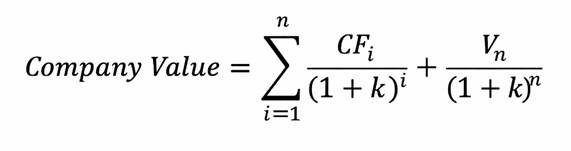

Valuing a company through discounted cash flow (DCF) consists, in simple terms, of bringing future cash flows to present value plus a terminal value.

This is the formula:

CFi: Cash flow in year “i”. This is what the company generates through its operations.

Vn: Terminal value in year “n”. Based on the company’s long-term growth expectations, this value is calculated. “n” is subjective—it could be year five, for example[2].

K: Discount rate applied to these cash flows.

This discount rate is key in the current environment. It is subjective and depends on factors such as opportunity cost[3], expected growth, or the cost of capital, among others, depending on the perspective of the person performing the valuation.

For example, if the best available investment alternative has an expected return of 10%, or if I require a 10% return for a given investment due to its risk or duration, then k = 10%.

That said, can k change? Of course. It can increase if I perceive more risk in the investment, which reduces valuation (per the formula), as I demand higher returns. It can also change due to interest rate movements. Suppose I require a 10% return and assume a 5% spread over risk-free rates (which are at 5%). If risk-free rates rise to 7%, then k must increase accordingly. Since k is in the denominator, the company’s valuation decreases.

The war has had an immediate impact on markets, with declines in equities, as expected. However, what may be more relevant is the indirect effect via inflation and interest rates, which is more persistent and harder to reverse.

Returning to the DCF formula—and I promise this is the last headache—growth companies, particularly technology firms linked to artificial intelligence, are more affected for two reasons:

- Their cash flows are further in the future, so a higher k has a greater negative impact on valuation.

- They trade at demanding multiples, meaning expectations are already very high and therefore more vulnerable to disappointment.

We can see this in the chart: the light blue line (Magnificent 7) falls by 12%, the dark blue line (traditional S&P 500) falls by 4.6%, and the beige line (S&P Equal Weight) rises by 0.19%.

Source: Facset Research Systems Inc.

This highlights concentration risk. When markets rise, it helps. But when conditions deteriorate, it becomes a vulnerability—especially in uncertain environments.

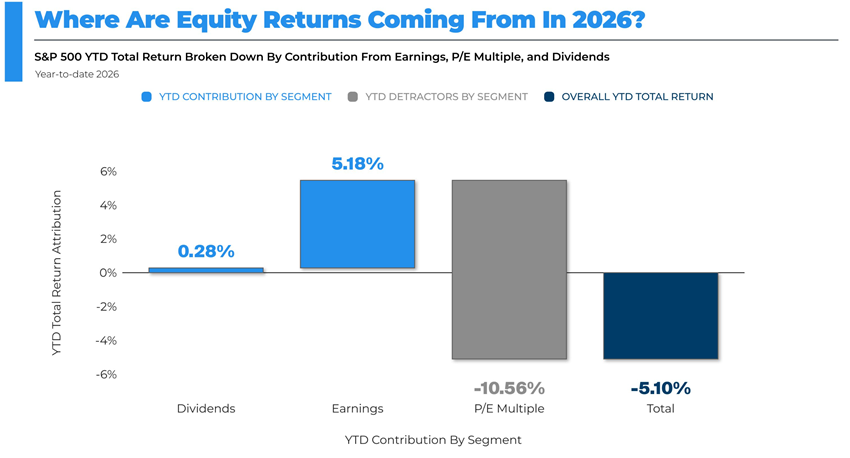

That said, although it may still be early, corporate earnings have not been significantly affected. The declines are driven more by uncertainty, as shown in the decomposition of the S&P’s performance: dividends contributed +0.28%, earnings +5.18%, and the multiple (P/E) -10.56%, which ultimately dragged the index down.

Source: Facset Research Systems Inc.

The P/E ratio is equal to price divided by earnings. If price rises while earnings remain constant, the multiple expands, reflecting investor optimism—and vice versa. We do not know what will happen with the war, inflation, or interest rates, but many investors prefer not to wait and sell amid rising uncertainty. Higher uncertainty, lower multiples.

Private credit funds

When asked about the impact of war on financial markets, the immediate reaction is concern, risk, and uncertainty, which naturally leads many investors to sell. Beyond the human tragedy, from a financial perspective, what is more concerning is rising inflation, potential interest rate hikes, and the consequences for leveraged structures that are not immediately visible.

Some worrying news has emerged regarding private credit funds. These funds lend directly to companies and have grown significantly since 2008, partly due to tighter banking regulation. It is a less transparent market, but increasingly relevant.

Many loans are floating rate, meaning companies that borrowed when rates were low are now paying interest rates of 9–10%, leading to refinancing difficulties and rising defaults—although not always officially recognized, as they are often masked through extensions, restructurings, or PIK payments[4].

In addition, these funds have financed small and mid-sized software companies, a sector now threatened by artificial intelligence, which may deliver similar solutions faster and at lower cost.

This creates a combination of risks: higher financing costs and declining revenues.

It is no coincidence that many investors are requesting redemptions. Some semi-liquid funds are limiting or even suspending withdrawals, while banks tighten financing conditions.

This reveals a key fragility: many funds offer liquidity while investing in illiquid assets. These mismatches only become visible in stressed environments.

This situation somewhat resembles 2008. After years of low interest rates, complex structures with questionable assets were created. When rates rose, the fragility of the system became evident.

Today’s situation is different—less leverage, more capital, simpler structures—but the underlying dynamics are similar. Key risks include opaque valuations, concentration in software/technology, and exposure to semi-liquid vehicles.

This once again reminds us of a very human tendency: repeating mistakes. In times of prosperity, greed blinds us and pushes us to take on more risk. We believe we will know when to exit, that we will stand up just before the music stops. But reality is often different.

The music always stops. The question is whether we are already seated… or still standing when it does.

For more content, click here.

[1] If I am lent 100 to repay in one year and inflation over that year has been 10%, I repay the same 100, but it is worth 10% less (a very simple example for training purposes).

[2] The terminal value is calculated as follows: Vn = (CFn / (k − g)), where k is the discount rate and g is the expected perpetual growth rate, which is usually similar to global GDP growth. No company grows above GDP indefinitely.

[3] Opportunity cost can be defined as the expected return of the best available investment alternative.

[4] Payment In Kind (PIK): the company stops paying interest in cash and instead capitalizes it by adding it to the debt. When a company is under financial stress, this provides short-term relief, but it increases overall indebtedness.