In April, equity markets rose sharply worldwide, including in emerging markets. In the fixed-income market, performance was mixed: on the one hand, government bonds fell due to rising inflation expectations, while corporate bonds rose thanks to strong corporate earnings.

- S&P 500: +10,49%

- Nasdaq: +15,66%

- Stoxx Europe: 5,56%

- MSCI All Country World Index (EUR): +8,53% (The dollar fell 1.53%, the index in USD rose 9.52%).

- Global Fixed Income Index (EUR): -0,55% (The dollar fell 1.53%, the index in USD rose 0.30%).

Despite ongoing tensions in Iran and issues in the Strait of Hormuz, with oil prices exceeding $110 per barrel, optimism returned to the market thanks to renewed interest in artificial intelligence companies, strong first-quarter earnings (84% of companies beat expectations, well above average), and perhaps hopes for a lasting ceasefire.

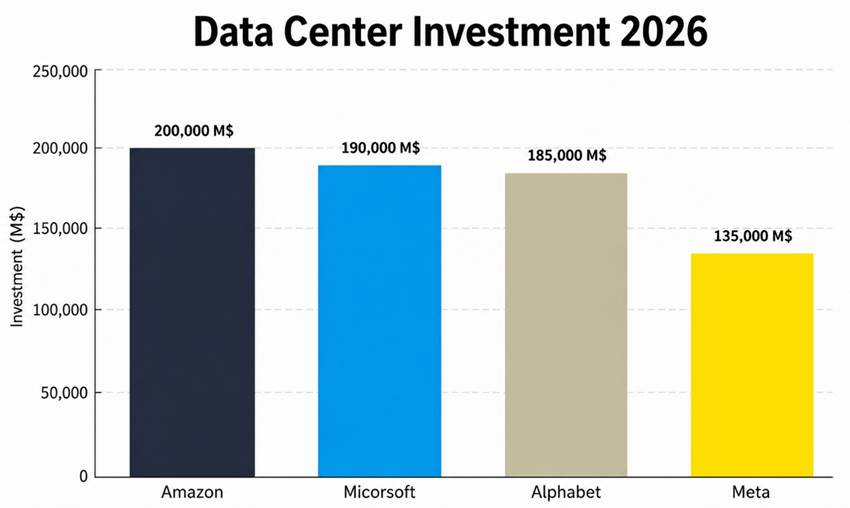

Optimism has returned to the artificial intelligence sector with the announcement of new investments in the construction of new data centers. This image shows the investment forecast from these companies.

Source: Seeking Alpha

These announcements have triggered sharp rallies in one of the most important suppliers to data centers: semiconductors. This sector has risen by nearly 50%,[1] which has boosted the indices. Optimism is returning, but doubts remain: will they deliver on these gains? I don’t have the data to know whether they will or not, but if they fall short, the declines will be steep given the high price-to-earnings multiples.

Geopolitics

The situation in Iran is currently marked by high tension, though it is far from a full-scale open war. Following a recent phase of attacks between Iran, the United States, and Israel, the conflict has entered a sort of fragile truce, marked by diplomatic negotiations.

Despite this attempt at de-escalation, the risk of new clashes remains high. The most sensitive point continues to be the Strait of Hormuz, key to global oil trade, whose stability directly influences global markets.

In this context, the United States seeks to avoid a prolonged war and contain Iran’s nuclear program, while Israel maintains a firmer stance. For its part, Iran, though weakened, retains the capacity to respond.

In short, we are not facing an all-out war, but rather a very unstable balance, where any incident could reignite the escalation.

Europe

One of the first economic consequences of the war has been a surge in energy prices. Europe has been one of the hardest-hit regions, due to its status as a net energy importer. Although European markets showed some recovery, it was more moderate than in other regions. Against this backdrop, the European economy barely managed to grow in the first quarter, as the conflict in the Middle East has derailed a long-awaited recovery.

The latest European data offers little cause for optimism, such as consumer confidence falling by 20.6%, —the worst reading since 2022 according to the European Commission— and an April PMI[2] (Purchasing Manager Index) of 48.6, below the 50-point threshold that separates expansion from contraction. The contraction stems from both the services and manufacturing sectors, with data pointing to inflationary pressure.

This is Europe’s perennial problem: excessive regulation and an ideologically driven industrial policy that has weakened its defenses against external shocks. Instead of strengthening its domestic energy capacity, it has remained exposed to instability in external supply, such as from the Middle East or Russia.

The weaker performance of European companies is consistent with this perspective. Companies operating in an environment of heavy regulation, high tax burdens, and energy uncertainty face greater difficulties competing with their U.S. counterparts.

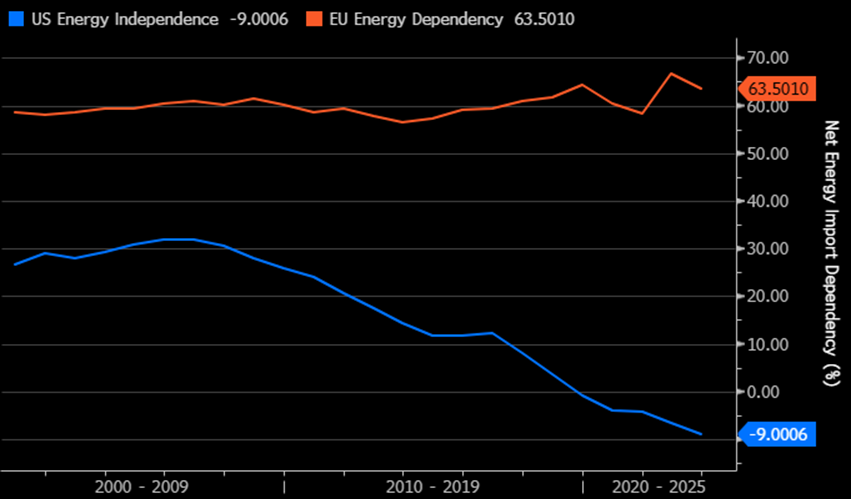

Source: Bloomberg

This chart shows the degree of energy dependence in different regions. While Europe meets nearly 60% of its needs through imports, the United States is in the opposite situation, with exports exceeding imports.

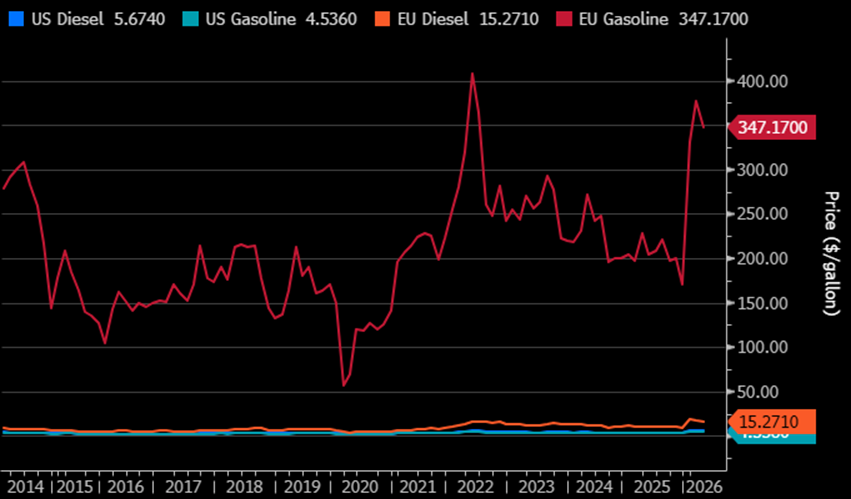

This difference is clearly reflected in the prices paid by both economies, as shown in the following charts. The gap in energy costs faced by European businesses and households is particularly significant.

Source: Bloomberg

Source: Bloomberg

And it’s not just a matter of price differences, but also of greater volatility. In such an environment, how can a company plan its investments, costs, or margins with so little visibility? Competing under these conditions makes many European companies true heroes.

Therefore, in the face of any external shock, Europe reveals its fragility, and this has been demonstrated once again. There are very good companies in Europe—as good as or better than their American counterparts—but they are at the mercy of political whims.

Inflation

Yeah, I know, I’m obsessed with this topic, but how could I not be? They call it the “invisible tax” because it takes your money without you even noticing—except for a friend’s mom, who used to tell us, “I don’t care if prices go up; I’m always going to put 20 euros’ worth of gas in my car.”

To give you an idea, central banks aim for 2% inflation—great—but with that rate of inflation, purchasing power drops by 50% over 36 years. If you want to leave your wealth to your children, it’s clear what you need to do if you want them to be able to buy the same things—and I’m not talking about luxuries.

Is an annual inflation rate of 2% good or bad? If monetary policy is more or less stable, it can be positive, but there are economies that have maintained low inflation rates—such as Switzerland, with an average inflation rate of 0.6% this century—where the population has maintained high purchasing power compared to other countries. Someone might rightly point out that Japan has had an average inflation rate of 0.5% over the same period and hasn’t fared well. The difference lies, I believe, between sound monetary policies and excessively interventionist ones, but I didn’t want to focus on this discussion, which could be interesting for a later commentary.

On the other hand, do we really believe that current inflation is 2%?

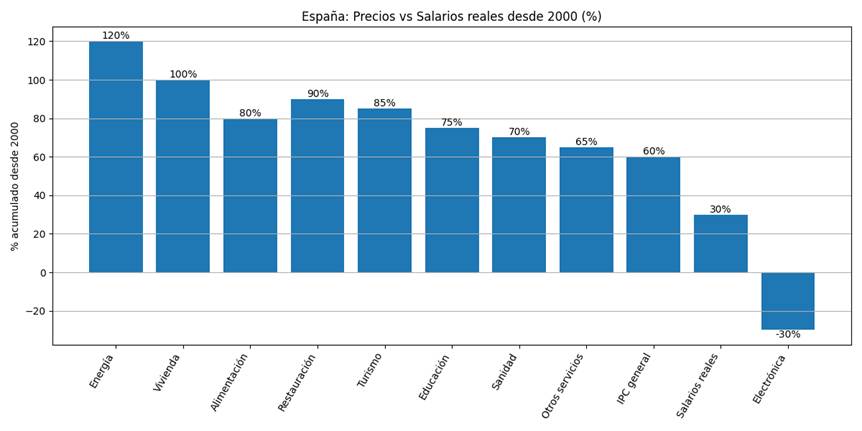

Source: INE, Chatgpt

How is it possible that CPI-measured inflation has averaged 60% since 2000, while many essential goods and services—such as education, healthcare, food, energy, and housing—have risen far beyond that? The CPI is an average calculated from a basket of goods and services with specific weightings. Is it designed to produce a “pretty” result? Not necessarily, but it certainly falls short of the reality of the bills a family faces in their daily lives.

Does this mean the data is incorrect? No. But it does mean the indicator has significant limitations. For example, electronics, which have seen price drops or quality improvements, help keep the index in check, even though their share of household spending is small and they are not essential. In contrast, categories such as food, housing, education, and healthcare—which are far more relevant to families’ well-being—have seen much higher increases.

The result is clear: even though the CPI reflects a moderate rise, the inflation that many families actually experience is higher, especially when their wages have not grown at the same pace in real terms.

Electronics prices are falling—in other words, there is deflation. This concept has become almost taboo, as if it were inherently negative. However, its impact depends entirely on the context.

In an uncertain environment, where consumption and investment are contracting, falling prices are often a sign of weakness: companies lower prices to move their inventory, even if it means accepting lower margins or losses. This type of deflation can create a vicious cycle of reduced economic activity. Take Japan, for example.

But there is another, much healthier form of deflation: that which stems from productivity gains. When a company is able to produce more efficiently, it can lower prices without eroding its margins. In that case, falling prices are not a problem but a blessing; purchasing power increases, and money “goes further.” Take Switzerland, for example.

The risk we face today is not just a spike in inflation, but the possibility that it will coexist with low economic growth—that is, a scenario of stagflation, a word no economist wants to hear. Such situations are typically triggered by a supply shock in a context of economic weakness, often preceded by prolonged periods of excessive monetary stimulus.

Let’s hope the conflict ends soon, as we all wish. However, it’s worth noting that the problem lies not only in the war, but in the imbalances that had built up beforehand—imbalances that the conflict has merely brought to light. An environment of excessive policies and regulations, coupled with ongoing monetary stimulus, has gradually eroded the economic strength of these countries.

Given this situation, there is no choice but to keep investing so that inflation doesn’t erode your purchasing power. There will surely be volatility and there will be downturns that, at least for me, I won’t be able to predict, but I do know that if you stay invested and let the companies do their job, the rewards will come.

Following up on that last paragraph, I’d like to wrap up this post by giving you a choice between the following two options (it’s important to answer with the first thing that comes to mind):

- Receive €1 million today

- Receive €0.05 today, which doubles every day for 30 days, that is:

- Day 1: €0.05

- Day 2: €0.10

- Day 3: €0.20

Before answering, here’s a hint: our brains overvalue the immediate and undervalue the long term, especially when growth isn’t linear.

This is interesting for understanding how compound interest (compound returns) works in investing. Do the math and tell me if it isn’t worth being patient with investments—provided, of course, that you choose your companies wisely.

As Warren Buffett said: “The first rule of compounding: never interrupt it.”

For previous market reviews, click here.

[1] Measured by the State Street SPDR S&P Semiconductor ETF

[2] This is a survey conducted among corporate purchasing managers