In June, equities posted mixed results. Indices with the highest weightings in technology and growth stocks saw profit-taking, while more cyclical or defensive sectors—such as industrials, healthcare, and financials—performed relatively better. This factor largely explains why Europe outperformed the United States during the period.

Fixed income, meanwhile, performed somewhat better, especially in the longer-duration segments, supported by the decline in long-term interest rates. As you know, bond prices move inversely to interest rates. In contrast, short-term maturities performed less favorably.

- S&P 500: -1,06%

- Nasdaq: -0,19%

- Stoxx Europe: +2,51%

- MSCI All Country World Index (EUR): +1,32% (The dollar rose 1.80%; the USD index fell 0.92%.)

- Global Fixed-Income Index (EUR): +1.35% (The dollar rose 1.80%; the USD index rose 0.24%.)

Why did technology and growth stocks struggle this month?

The second quarter had been very positive for these types of companies, especially those most closely tied to technology, artificial intelligence, and structural growth. Following strong cumulative gains, many investors took advantage of June to take profits and reduce their exposure to the segments that had performed best.

Rather than a single trigger, the move appears to be driven by a combination of factors:

- Strait of Hormuz.

On June 14, a preliminary agreement was announced to reopen the Strait of Hormuz and lift the U.S. naval blockade, although its implementation was pending formal signing. Since then, the reopening has been taking place gradually and with great caution.

In practice, the lifting of the blockade does not imply an immediate return to normal maritime traffic. Significant issues remain to be resolved, such as mine clearance, safety guarantees for navigation, and the possible imposition of tolls or controls by Iran.

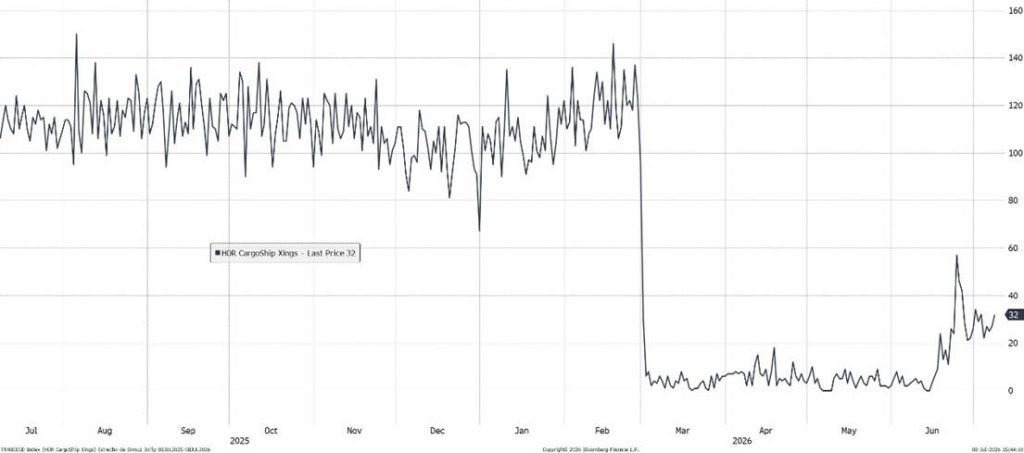

Although the agreement is positive news, traffic through the strait is still far from returning to pre-war levels, as can be seen in the image.

Source: Bloomberg

The number of ships passing through the Strait of Hormuz each day remains well below normal levels: about 32 vessels, compared to more than 100 under normal conditions. This situation reflects the fact that the United States and Iran have not yet reached a final agreement on the terms of the Memorandum of Understanding.

The lack of clear progress maintains a high degree of uncertainty, and as a result, the risk of further upward pressure on energy and other commodity prices remains. Reduced security in the region and tighter supply could lead to additional price pressures.

As of July 8, at the time of writing this commentary, President Trump declared that the agreement was terminated following new attacks linked to Iran in the Strait of Hormuz, which once again increases uncertainty regarding the normalization of maritime traffic in the region.

- Oil Price.

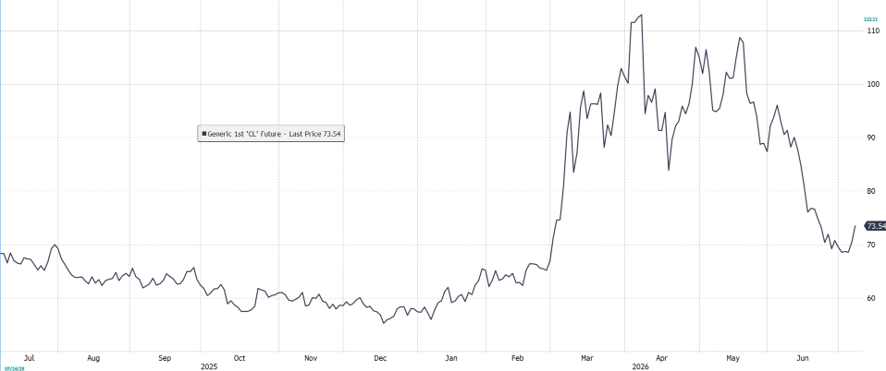

Since news began to emerge of progress toward the signing of a Memorandum of Understanding between the United States and Iran, the price of oil has corrected sharply, falling from levels near $100 per barrel to below $70.

This decline reflects the market’s anticipation of a possible gradual normalization of maritime traffic in the Strait of Hormuz and, consequently, a lower risk of disruptions to energy supplies. However, until the agreement is fully implemented and doubts about security in the region persist, the price of oil will remain highly sensitive to any news related to the conflict.

As shown in the chart below, the price of crude oil has experienced a sharp correction from the highs reached during the period of heightened geopolitical tension.

Source: Bloomberg

Furthermore, the United States’ strategic oil reserves have helped cushion the impact of the supply crisis so far. These reserves exist precisely for exceptional situations like the current one, in which there are significant disruptions in the energy market.

However, the United States cannot rely on them indefinitely. The cumulative decline in reserves, as shown in the chart below, makes it clear that this support mechanism has its limits. Therefore, if the situation drags on and supply does not return to normal, the market could once again face increased pressure on oil prices.

Source: Bloomberg

It is worth noting that these reserves refer to the total amount of crude oil available in the United States—that is, both commercial inventories and strategic reserves. The chart shows that the country’s oil “buffer” has shrunk significantly.

This means that the market has less of a safety margin against potential supply shocks. Consequently, any new disruption could have a more significant impact on crude oil prices.

- Inflation.

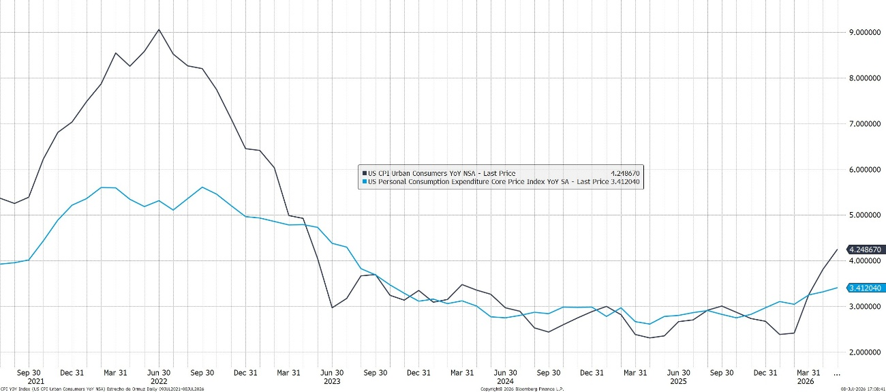

It seems clear that investors are not entirely comfortable with the trend in inflation. As noted earlier, the current environment remains marked by a high degree of uncertainty, particularly due to risks associated with energy prices and potential supply disruptions.

In this regard, the chart shows how both the CPI and the PCE (Personal Consumer Expenditures) have recently rebounded, reinforcing market concerns about the possible persistence of inflationary pressures. This scenario could limit the Federal Reserve’s room to maneuver and delay future interest rate cuts.

Source: Bloomberg

Although the main factor behind the rise in inflation has been the increase in energy prices, there are other factors that are also putting pressure on the macroeconomic outlook. These include the persistent fiscal deficit, the strength of the labor market, and the acceleration of capital investment related to artificial intelligence.

Regarding this last point, Savita Subramanian of Bank of America noted the following: “Since November, most hyperscale companies have seen their metrics deteriorate: cash flow conversion has stagnated, the supply of investment-grade stocks and bonds has increased, share buybacks as a percentage of market capitalization have slowed, and capital expenditures as a percentage of operating cash flow for these companies are projected to reach nearly 100% by year-end, up from 40% in 2023.”

These companies’ investment forecasts continue to rise, supported primarily by two sources of financing: debt issuance and stock sales. This increase in capital spending is driving greater demand for equipment, infrastructure, and specialized services, which may put upward pressure on suppliers’ prices.

Here’s the key point: on the one hand, investment in artificial intelligence is driving demand; on the other, geopolitical tensions and disruptions in the Strait of Hormuz may limit supply and drive up the cost of energy and other raw materials. The combination of stronger demand and tighter supply may intensify inflationary pressures.

- Speech by Kevin Warsh, the new chair of the FED.

On June 17, the new Fed chairman, Kevin Warsh, announced that interest rates would remain unchanged, although investors perceived a slightly hawkish tone (suggesting a rate hike) as he focused on restoring the Fed’s anti-inflation credibility.

What inflationary risks might explain Warsh’s cautious tone? The recent spike in inflation likely led Warsh to repeatedly emphasize price stability as one of the Federal Reserve’s primary objectives. Furthermore, it is worth remembering that 2026 is an election year in the United States, and voters tend to react particularly negatively to rises in energy and food prices.

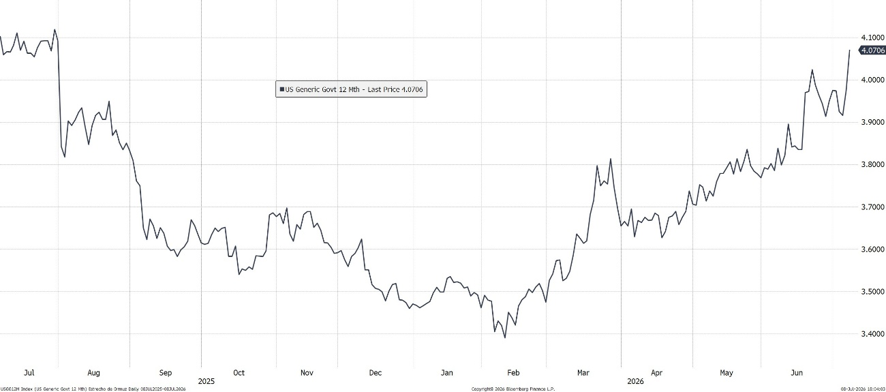

The market has priced in this message, particularly through a rise in yields on short-term maturities, which implies a decline in the price of those bonds. The chart shows the yield on the 1-year U.S. Treasury note, which has risen significantly since the start of the war.

Source: Bloomberg

This rise reflects market expectations regarding interest rate trends over the next 12 months. Therefore, when the yield on the 1-year Treasury note rises, it typically indicates that investors are pricing in the possibility that the Fed will keep rates high for longer—or even that it might be forced to raise them again.

However, a particularly interesting development has occurred this month. The following chart compares the yield on the 1-year U.S. Treasury bond—represented by the dark blue line—with the trend in oil prices—represented by the light blue line.

Source: Bloomberg

The curious thing is that, when oil prices rise, interest rates quickly follow suit due to fears of a spike in inflation. However, when oil prices correct, interest rates do not fall back with the same intensity.

Why does this happen? Probably because the market is not viewing the movement in oil prices as an isolated factor, but rather within a broader context of inflationary uncertainty. Even though the price of crude oil has fallen, other risks remain: geopolitical tensions, lower reserve buffers, fiscal pressure, a strong labor market, and heavy investment in artificial intelligence.

In other words, interest rates seem to be sending a message: the ultimate impact on inflation and monetary policy is still unclear. As Eric Robertsen of Standard Chartered noted:

“Oil-related volatility may have subsided, but we expect it to be replaced by interest rate and currency volatility in the second half of the year. Enjoy this respite; in our view, it is likely to be temporary.”

- But, What happened to the gold?

If investors anticipate higher interest rates, the opportunity cost of holding gold increases, since gold does not pay coupons or generate periodic income. Conversely, if a short-term U.S. Treasury bill offers an attractive yield, holding gold becomes less appealing, especially if real yields also rise.

That said, the price of gold has fallen by approximately 25% from its January high and is down nearly 6% year-to-date. The strength of the dollar has been a major headwind, but supportive structural factors remain in place: central bank purchases, interest in gold-backed assets, and high government spending. The question, therefore, is whether this correction might represent a buying opportunity.

Finally, I’d like to discuss SpaceX’s initial public offering (IPO) and how it might impact both passive and active investing.

This company, founded by Elon Musk, went public on June 11 and, in just a few days, became the fifth-largest company in the world, surpassing even Amazon in market capitalization. Additionally, it is expected to be added to the Nasdaq index soon.

This move comes amid a period of strong activity in the IPO market, particularly among companies involved in artificial intelligence. Many companies are capitalizing on the high level of investor enthusiasm for the sector and very high valuations. In practice, an IPO involves the sale of shares to the public by founders, partners, or existing shareholders. When valuations are attractive, these shareholders may see a favorable opportunity to monetize part of their investment.

In this same context, the market is also anticipating potential IPOs by Anthropic and OpenAI, two of the most prominent companies in the artificial intelligence ecosystem and highly attractive to investors.

How does this affect passive management? If these companies are included in the major indices, they will be assigned potentially significant weightings, forcing index funds to purchase them in proportion to their market capitalization. This can generate very significant buying flows and increase the indices’ concentration in a small number of companies.

Furthermore, the rise of passive investing and constant benchmarking have changed the way risk is measured for actively managed funds. A 5% position in Nvidia may seem high in absolute terms. However, if Nvidia accounts for about 7.9% of the S&P 500, that 5% means the fund is underweight relative to the index. In this context, if the company continues to post strong gains, the fund could lag behind its benchmark—not because it lacks exposure to that company, but because its weighting is lower than that of the index itself.

At Altum, we believe it is more prudent to invest in equally weighted indices—where all companies have the same weighting—rather than relying excessively on a small group of companies, many of which belong to the same sector. Even though these companies have performed exceptionally well recently, their growing weight in the indices adds a concentration risk that we consider unnecessary.

Read here our latest Market Reviews.